Market Flash Report | March 2024

Economic Highlights

United States

- U.S. employers added a better-than-expected 275,000 new jobs to the economy in February, ahead of the 198,000 estimate. The unemployment rate ticked higher to 3.9% from 3.7% in the prior month. Downward revisions to December and January reduced initial estimates by 167,000 jobs. Wages grew 0.1% M/M in February, slightly below the 0.2% expectation. Wages grew at an annualized clip of 4.3%, which is higher than the rate of inflation. This report showed mixed signals with this month’s better number offsetting downward revisions to the prior two months, and wages were still hotter than the Federal Reserve would like to see.

- According to the Fed’s preferred inflation gauge, the Core Personal Consumption Expenditures, or Core PCE, inflation rose 2.8% Y/Y in February or 0.3% M/M. Core PCE increased in line with economist expectations, while headline PCE came in slightly below expectations. Headline PCE increased 0.4% M/M or 2.5% Y/Y. A report on consumer spending surged 0.8% M/M.

- All eyes have been on the Fed and their next move regarding monetary policy. After pricing in six or seven rate cuts to start the year, market expectations have come down sharply, now matching the Fed’s dot chart showing three rate cuts in 2024. The Fed Fund Futures expect the first rate cut to occur at the June meeting.

- Retail sales in the U.S. were up 0.6% M/M in February 2024, following an upwardly revised 1.1% fall in January. The relatively modest increase, combined with a larger decline in January, suggests a potential slowdown in consumer spending. The biggest increases were seen in sales at building materials and garden equipment (2.2%), motor vehicles and part dealers (1.6%) and electronics appliance stores (1.5%).

- Durable goods orders rose 1.4% M/M in February after declining 6.9% in the previous month. Orders rebounded for transportation equipment (3.3% vs -18.3%). Excluding transportation, new orders increased 0.5% and excluding defense, new orders increased 2.2%. Orders for non-defense capital goods excluding aircraft, a closely watched proxy for business spending plans, increased 0.7% after a 0.4% decrease in January.

Non-U.S. Developed

- While the eurozone economy remains fragile, it appears to have stabilized in March based on the Flash Composite Purchasing Managers' Index (PMI). The reading of 49.9 was just below the key 50 level and was a 9-month high. A modest recovery of service sector output gained momentum, accompanied by a softening in the rate of manufacturing output decline. However, ongoing decreases in output in France and Germany offset a gathering upturn in the rest of the eurozone, pointing to an uneven economic picture.

- Inflation in the eurozone hit a 3-month low of 2.6% in February, with the core rate sitting at 3.1%. Both readings remain above the European Central Bank’s 2% target, and most of the increase came from the services side of the economy. Given the weakness in eurozone economic activity and tamer inflation, the ECB could begin to cut rates soon to stimulate growth.

- Japan’s economy narrowly avoided a recession with 0.1% GDP growth reported in Q4. A strong upward revision in consumer spending provided the boost. Private consumption, which accounts for about 60% of the economy, shrank for the third straight quarter, due to elevated cost pressure and persistent headwinds at home.

Emerging Markets

- China’s factory activity in March expanded by its strongest pace in more than a year. The Caixin/S&P Global China Manufacturing PMI was 51.1 in March, its strongest since February 2023 after coming in at 50.9 in February. This reading on manufacturing was consistent with the official National Bureau of Statistics Manufacturing PMI, which came in at 50.8 in March.

- One continued concern for China is potential deflation and falling prices. Producer prices have declined for well over a year while consumer prices have declined for four of the past five months.

- Growth in the Chinese services sector hit a 9-month high in March based on the official Non-Manufacturing PMI. The headline reading of 53.0 was well ahead of the 51.4 reading in the previous month.

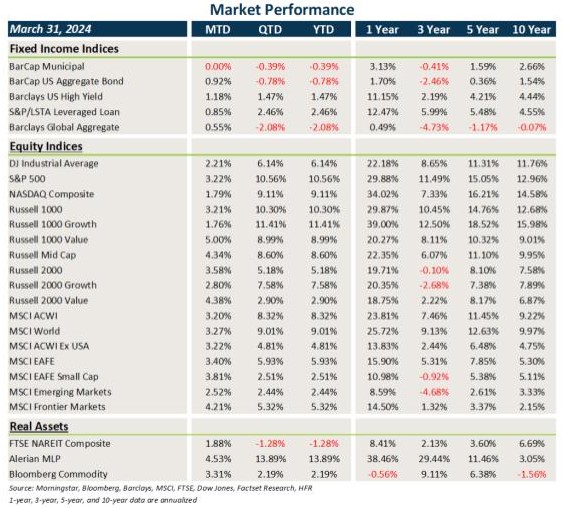

Market Performance (as of 03/31/24)

Fixed Income

- Treasury and other sovereign debt yields fell across the board in March, creating a small tailwind for core fixed income. Municipal bonds were flat last month, as the asset class is often technically driven.

- Credit spreads continued to tighten in March, fueling gains in HY, floating rate loans and EMD.

- The U.S. dollar weakened in March, providing another tailwind for non-U.S. assets.

U.S. Equities

- U.S. equity markets remained resilient in March, led by solid gains in small caps and value stocks. The Nasdaq was the laggard, but still gained 1.8%.

- Small caps beat large caps last month and value stocks outpaced growth stocks across all market caps.

- U.S. equities ended Q1 with some of the best quarterly gains ever.

Non-U.S. Equities

- Non-U.S. equities generally outperformed U.S. equities in March, led similarly by small caps and value stocks.

- While small caps slightly outperformed large caps, value beat growth within EAFE markets by about 200 bps.

- Emerging markets lagged developed markets last month, dragged down by weakness in Eastern Europe, Latin America and China.

- Currency provided a boost to non-U.S. equities.

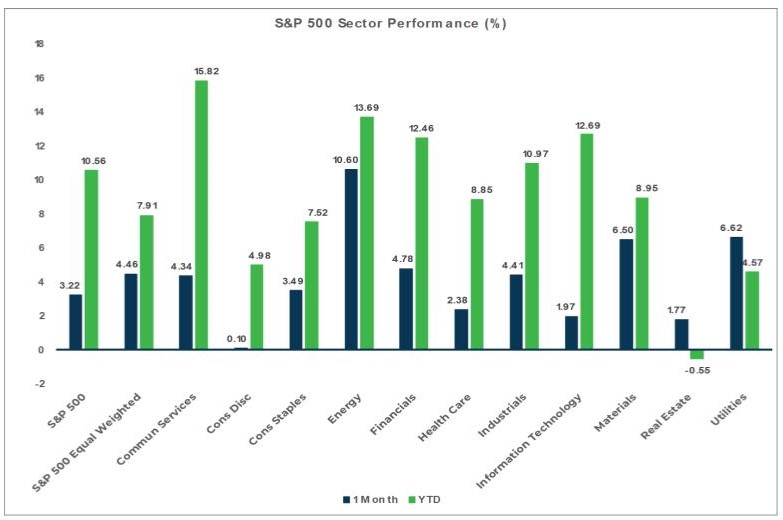

Sector Performance - S&P 500 (as of 03/31/24)

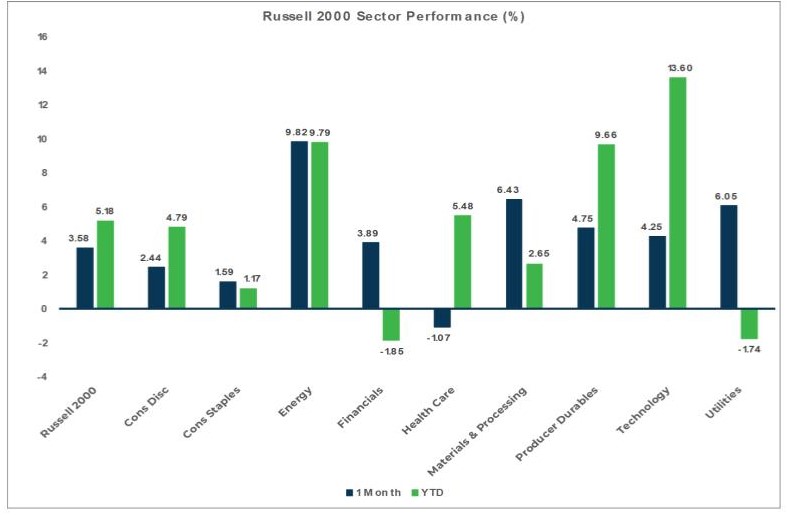

Sector Performance - Russell 2000 (as of 03/31/24)

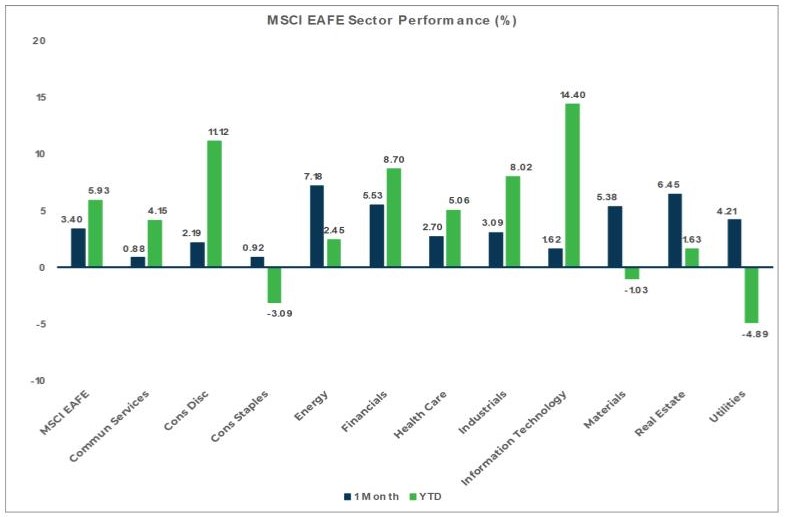

Sector Performance - MSCI EAFE (as of 03/31/24)

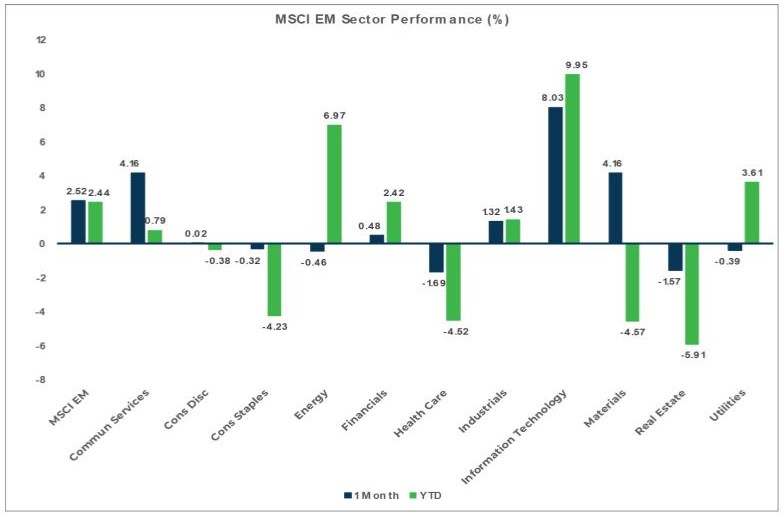

Sector Performance - MSCI EM (as of 03/31/24)